A recent BESS system integrator ranking from Rho Motion demonstrates how the energy storage industry is rapidly evolving as it grows. From 2023 to 2024, BESS shipments grew by 79%, and growth in 2025 is expected to be bigger. Data from the first half of 2025 (H1 2025) shows shipments have already surpassed the total for 2023 by 25%, highlighting the rapid pace of industry growth.

At the same time, as the industry expands and new players enter the market, smaller companies are steadily capturing market share. Meanwhile, the competitive dynamic is shifting between vertically integrated cell-and-system players and dedicated system manufacturers.

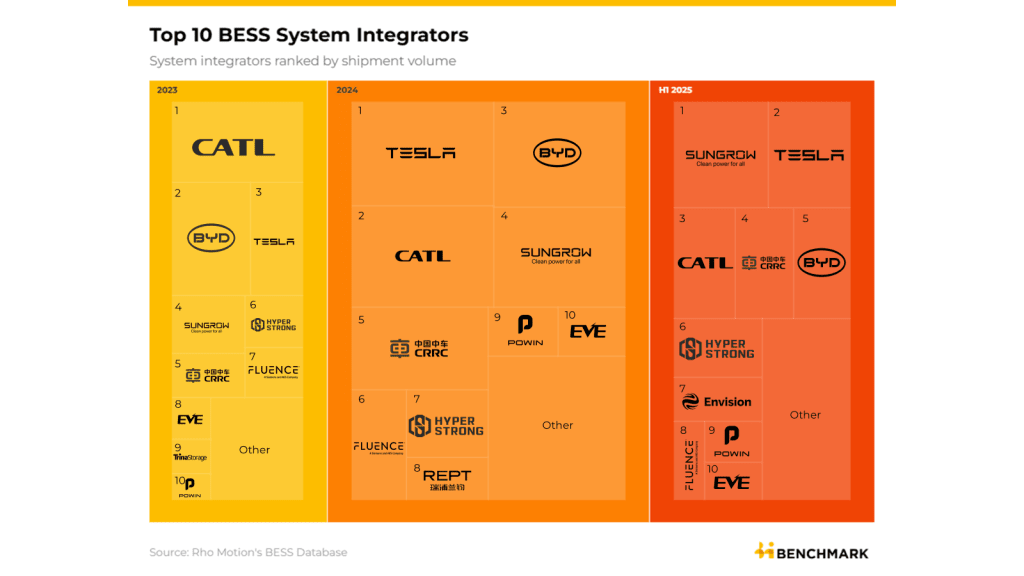

A market increasingly fragmented

In 2023 the top ten players accounted for 82% of the market, compared to 77% in H1 2025. Although the market remains relatively top-heavy, these dynamics are shifting as smaller players outside of the top five capture an increasingly larger portion of the market.

As well as this, market share across top players is becoming more balanced. In 2023, the leading player, CATL, held 20% of market share, compared with only 6% for the fifth-ranked, CRRC. In H1 2025, this gap narrowed to 14% and 9% respectively between Sungrow Power and BYD, ranked first and fifth. A lead that is far less pronounced as the landscape becomes more competitive.

System integration ability is proving more important

The competitive importance of system integrators has risen significantly as the market advantage of cell manufacturers has shown signs of weakening.

In 2023, cell makers accounted for at least 40% of BESS shipments, largely due to the surge in LFP cell prices in 2022. This gave cell players the advantage of being able to produce systems at lower costs, since cells made up the largest cost component of BESS systems.

By H1 2025, cell manufacturers’ share in the system market had dropped to below 30%. This shift has been fuelled by falling cell prices and the expansion of the battery industry, which has brought in more players and broadened the range of options available to BESS system producers, allowing them to compete more with vertically integrated players.

However, it is worth noting the growing importance of quality. As BESS players gain more experience operating projects, companies are increasingly recognising that, beyond initial costs, system integration capability plays a crucial role in long-term profitability. Factors such as operating lifetime, maintenance expenses, and insurance premiums all improve significantly with better system integration.

Cell supply sees more specialised players

On the cell side CATL continues to dominate the market but more specialised BESS cell players are taking market share. In H1 2025, Hithium and EVE Energy joined CATL in the top three cell suppliers for the BESS market overtaking the likes of BYD, which has steadily fallen to fifth position for BESS cell supply. H1 also saw nine cell players ship over 10 GWh of BESS cells.

The data behind this analysis comes from our BESS Monthly Database, which provides a project-by-project status update of grid-scale stationary storage projects. Click here to find out more.