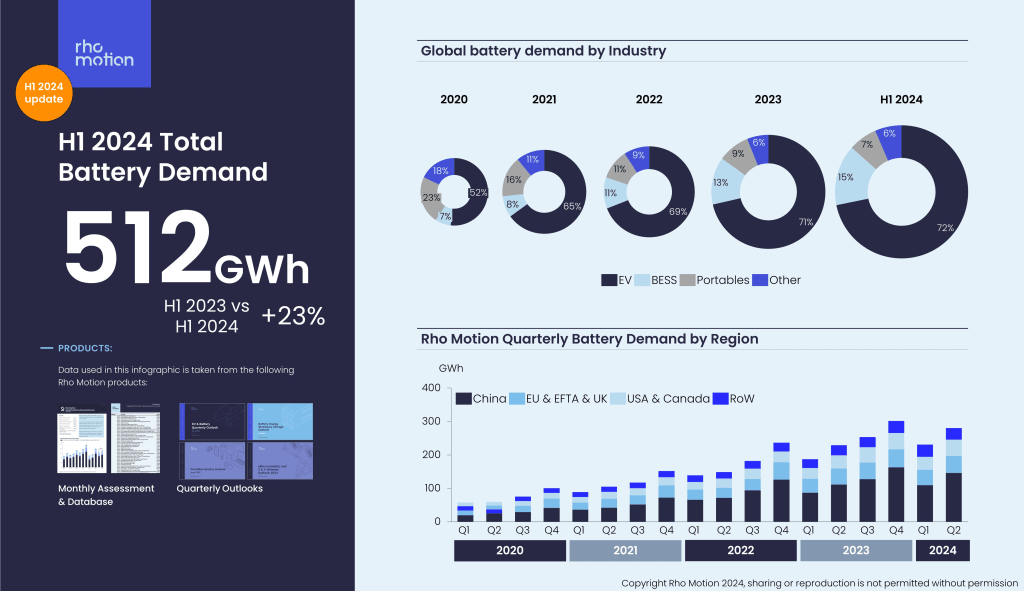

Battery Demand in H1 2024 exceeded 510GWh across all end use markets, an increase of 23% compared to last year revealed research house, Rho Motion, today. EV Battery demand accounted for 72% of this, with EV sales reaching seven million units in the first half of the year. The stationary storage market saw the strongest y-o-y growth of close to 50%.

Iola Hughes, Head of Research at Rho Motion, said:

“Amongst so much battery market negativity, the real upside of the year is the stationary storage market which is growing faster than the EV battery market. This is due to the frequency and size of projects entering operation increasing as more markets open themselves up to storage. The battery market is on track to surpass the 1.2TWh mark by the end of the year across all end-uses.” “Amidst the EV & battery slow down, cell manufacturers are being impacted, with Chinese players typically faring much better than their Korean and Japanese counterparts. In the first half of 2024 LG Energy Solution, SK On and Panasonic all saw their batteries deployed in EVs fall compared to H1 2023 as EV slowdown hits them the hardest. This comes at a time of raised concern from a number of these players, with SK On declaring a state of ‘emergency management’ this week.”

At a regional level China grew 29% y-o-y, accounting for just under 50% of global battery demand this quarter. In the US & Canada, y-o-y growth was 23% with battery demand in the stationary storage market more than doubling. The weakest growth was seen in Europe, increasing just 8% y-o-y, with notable decline in EV sales seen in Germany, Italy, Sweden and Switzerland

In the EV market in the first half of 2024 has grown by 20% globally and yet regional growth in Europe has slowed considerably down to 1%. Meanwhile in China there was a 30% year on year increase in EV sales and 10% in North America.

In terms of the battery manufacturer landscape, Rho Motion noted a large spread of growth rates in the first half of the year with Chinese players typically faring better than their Korean and Japanese counterparts. This comes at a time of raised concern from a number of these players, with SK On declaring a state of ‘emergency management’ this week.

| Cell Manufacturer | Growth H1 2024 vs H1 2023, kWh deployed in PC & LDV BEV & PHEV |

| CATL | +19% |

| BYD | +35% |

| LG Energy Solution | -8% |

| SK On | -4% |

| Samsung | +26% |

| CALB | +55% |

| Panasonic | -11% |

| Hefei Guoxuan High-tech Power Energy | +17% |

| Sunwoda | +64% |

| SVolt | +78% |

Looking at battery technology in the EV market, LFP (Lithium Iron Phosphate) continues to dominate the market in China, and NCM (Lithium nickel manganese cobalt oxides) outside of China. We witnessed LMFP and sodium ion batteries enter the mix in the final months of 2023 and are now seeing low, but consistent, sales of EVs with these batteries.

In the stationary storage market over 75GWh of new capacity entered operation, more than in the whole year in 2022. Over 500 grid-scale projects entered operation in H1 2024, four of which were larger than 1GWh, with the largest a 1.4GWh project in California. In 2024, there are 18 projects over 1GWh planned to enter operation, compared to just four that entered operation in 2023.

A similar picture of cell manufacturer competition is seen in the storage market, with the skew of growth much higher towards Chinese players due to the popularity of cheap LFP cells in storage, ultimately leading to a continued decline in market share for the Korean cell manufacturers, who at present do manufacturer LFP at scale. In China, four sodium ion battery projects came online in the first half of 2024, as well as the first semi-solid state battery projects.

For the full year 2024 battery demand across all end use markets is set to increase by 20-25% y-o-y compared to 2023, which was the first year to surpass the 1TWh battery demand mark.

If you are a journalist and would like to hear more about our research and analysis, get in touch via our press office email: press@rhomotion.com.