The EU has revealed it plans to implement provisional countervailing duties on Chinese made EVs. This follows the result of an investigation that provisionally concluded “electric vehicle value chains in China benefit from unfair subsidies which is causing a threat of economic injury to EU BEV producers”. This decision comes just a month after the US introduced additional tariffs of its own to counteract Chinese competition.

Provisional tariffs

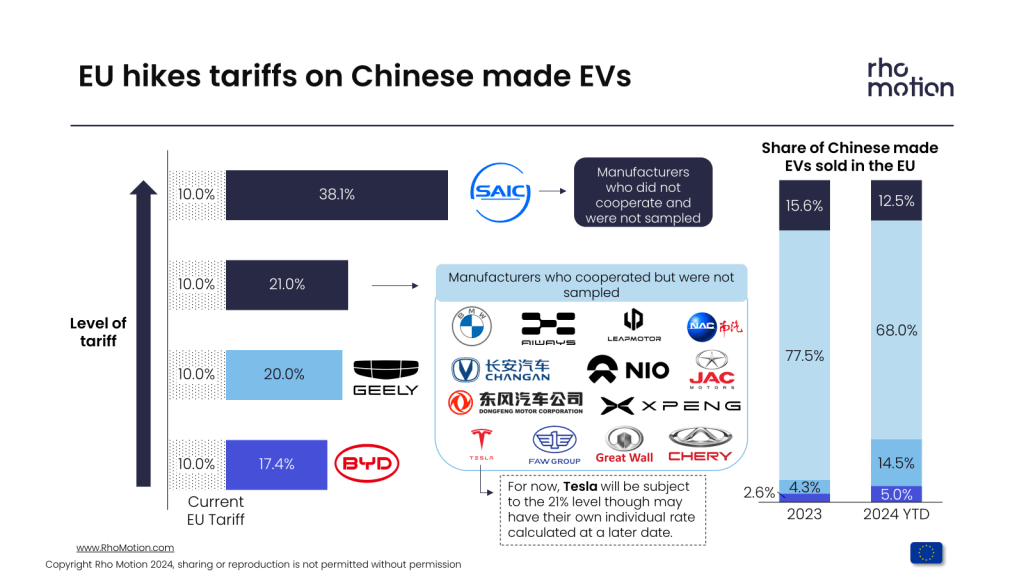

Currently the EU has a 10% import duty on BEVs; however, this is set to change. As a result of the Commission’s investigation into Chinese made vehicles it has released pre-disclosed provisional countervailing duties. The duties would be introduced from the 4th of July 2024, “should discussions with Chinese authorities not lead to an effective solution”.

Key Chinese OEMs BYD, Geely and SAIC would be subject to an additional 17.4%, 20%, and 38.1%, duties respectively.

Other OEMs who cooperated in the investigation but were not sampled will be subject to a 21% tariff, and the remaining companies who did not cooperate will be subject to a 38.1% tariff. For now, Tesla will be subject to the 21% level, though may have their own individual rate calculated at a later date.

The market

Nearly half a million EVs imported from China were sold in the EU in 2023, accounting for almost one-third of all EV purchases. This demonstrates the strong reliance the EU has on China for vehicle production. Subsequently it prompted the decision to impose tariffs on automakers importing from China, with the EU Commission arguing that Chinese EV manufacturers benefit from domestic subsidies, which give them an unfair advantage over their European competitors.

Rho’s Evaluation

Of the vehicles imported last year, 79% were from Western brands, predominantly Tesla, which accounted for over half of all the Battery Electric Vehicles (BEVs) imported but with significant volumes also from manufacturers such as Volvo (Geely owned) and Dacia. A further 15% of imports can be attributed to MG which, while a fully Chinese-owned company (SAIC), has brand heritage in the European market. Excluding those mentioned, the remainder made up just over 6% of EV imports into the EU last year.

Recent analysis from Rho Motion concluded that many of these Chinese-only brands such as BYD, MG and Great Wall Motors with scaled production in China have brought down production costs significantly. These low production costs allow additional profits of between 25% and 45% to be achieved over and above that already achieved in China, when operating logistics at scale in Europe.

This means the lower tariff levels will bring these manufacturers’ profits more in line with those achieved by European brands in the longer term, while likely not eliminating the profit margins completely. However, the higher levels of near 50% will be harder to overcome, particularly hitting MG whose low-priced models have been extremely popular among European consumers.

Will Roberts, Head of Automotive Research at Rho Motion, said: “European consumers are crying out for affordable EVs and with news today of sales plateauing in Europe, lower-priced vehicles will be critical to achieving the transition as planned. Having said that, Chinese manufacturers should be able to absorb some of these lower tariff levels into their generous profit margins.”

More Information

For more information on how our research can support you, get in touch.

Image credit: Adobe Stock

Read Rho Motion’s full analysis here.

Sources: European Commission