The future of how markets evolve is largely dependent on research and development (R&D). It drives innovation, competitiveness, and long-term growth. Within the automotive market, the role of R&D has gained increasing importance in recent years as the industry electrifies. When looking at the data of how much automakers invest in R&D there are large differences.

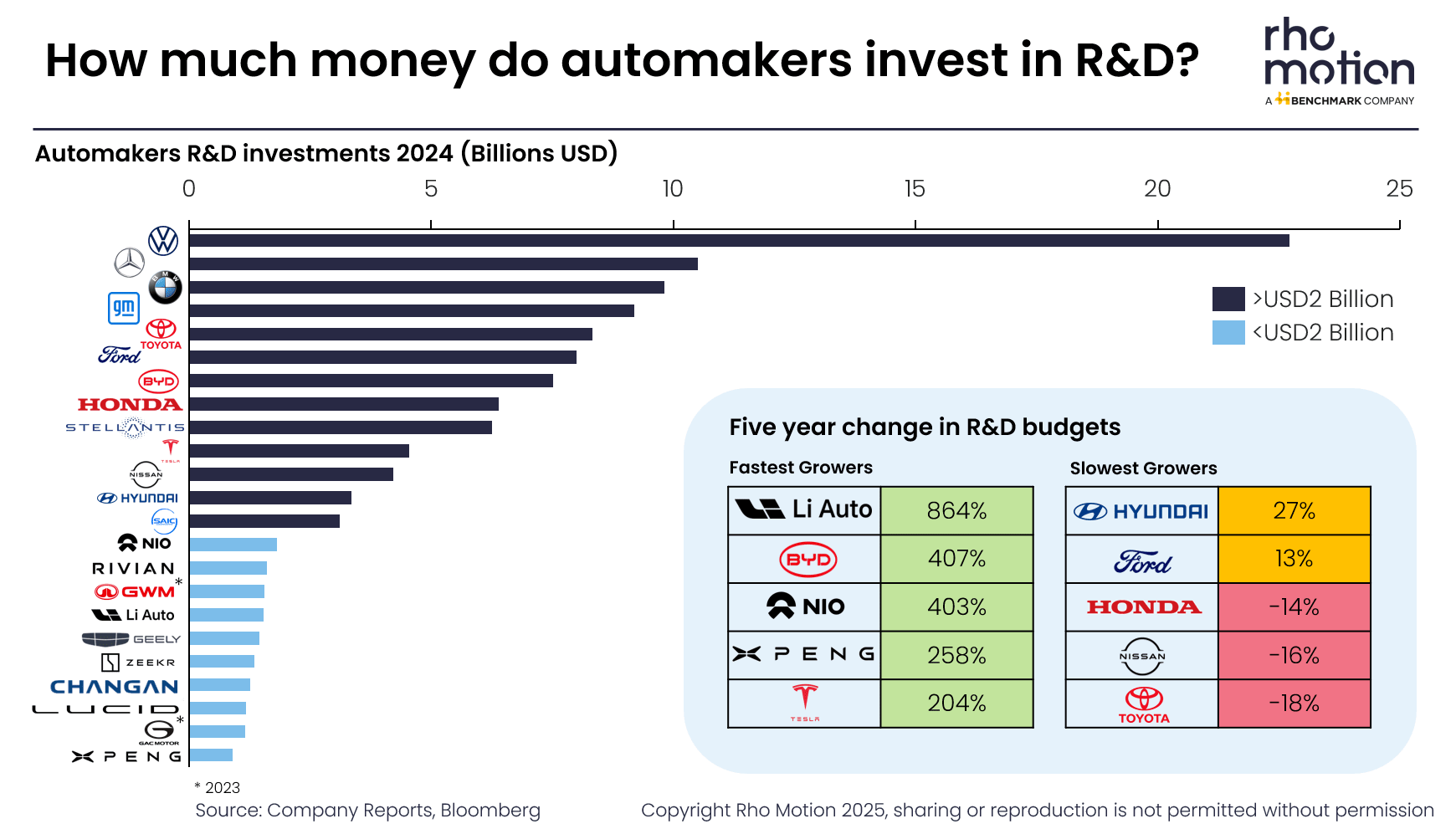

Why is VW the biggest spender on R&D?

In 2024, the VW Group spent just under USD23 billion on R&D, more than double the next highest spender, Mercedes-Benz. The R&D division has a focus on electrification, digitalisation, and sustainability including improving its modular electric platforms, software integration and development, and improving production efficiencies. Notably, a large part of its research still revolves around internal combustion vehicle (ICE) vehicle development as the group still sees it playing a large role in its future business.

Additionally, despite VW having its own software division, CARIAD, in which it has invested billions, it still partnered with, and invested in, Rivian last year to “speed up innovation”. This suggests that despite investing heavily in their own internal division, it was not producing the results wanted leading the business to look elsewhere.

Changing R&D budgets

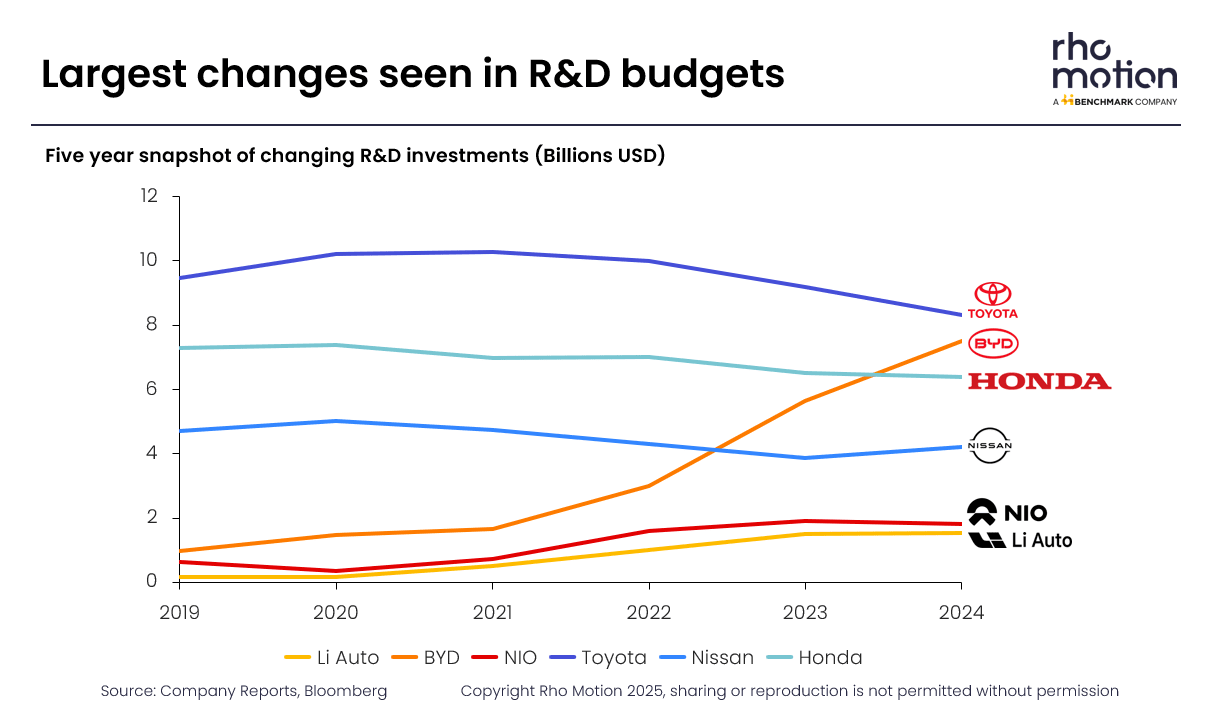

VW is a clear front runner for R&D budget size but when comparing R&D budgets over time, two key trends stand out. First, many Chinese EV manufacturers have significantly increased their investment in recent years, scaling up research efforts in line both with their own growth and the broader expansion of the Chinese EV industry. This reflects a strategic focus on innovation and technological leadership, which has been a hallmark of the Chinese EV market to date.

Meanwhile, the top three Japanese automakers—Honda, Nissan, and Toyota—have reduced their R&D budgets in recent years. Although their budgets remain substantial and higher than most other automakers, these players have sustained a strong emphasis on ICE technologies. As a result, EV sales still represent only a small fraction of their overall vehicle sales worldwide.

R&D in the future

Pure EV companies such as Tesla, BYD and NIO have the advantage of being able to focus all R&D resources on EV technologies. While legacy OEMs, that still produce ICE vehicles, are far more spread, as they continue to research ICE technologies.

While legacy OEMs will also research EVs, in the longer term the continuation of ICE research may affect their competitiveness in the EV industry as the vehicle market trends towards electrification.

More Information

For information about EV markets see our research or get in touch.

Image credit: Adobe stock