Over 140 countries have committed to net zero strategies, collectively covering 90% of the world’s total emissions. At the heart of this challenge lies the transport sector, accountable for approximately 20-25% of all global emissions. The bulk of these emissions emerges from road transport, encompassing cars, vans, buses, and trucks. The electric vehicle (EV) market is a cornerstone of the energy transition, with it playing a pivotal role in every country’s net zero ambitions.

Rho Motion has been tracking the EV market since the company’s inception in 2018, with its EV market analysis forming a central pillar of the company.

The transition towards EV marks the end of one epoch, the internal combustion engine (ICE) vehicle, and start of the next, the battery electric vehicle (BEV), with technologies such as plug-in hybrids (PHEVs) and range extended EVs (REEVs) playing a vital and supporting role in the transition. While growth in China remains strong, the adoption of EVs elsewhere is weaker. North America and Europe got off to a stronger start than other regions. However, they now sit finely poised with early adopters already transitioned to EVs, they must now encourage the remainder of the population to follow suit.

Other regions have their own barriers to overcome. With many still at an earlier stage of their energy transition, their issues involve changing public perception, overcoming range anxiety and scaling up charging infrastructure.

How did the EV and battery market evolve?

EVs first appeared in the 19th century with the emergence of the first automobiles, alongside internal combustion engine and steam power technologies. However, the mass production of ICE vehicles allowed for widespread availability and price drops for the public. This combined with the limitations of EVs such as short range, high cost, and lack of charging infrastructure, meant they could not compete on a practical level.

In the 1970s the appeal of EVs rose during the global oil crisis, governments and automakers began to seek alternative technologies. However, battery technology was still in its infancy. During the 1970s the lithium-ion battery was developed under sponsorship of Exxon Mobil, this in turn would form the foundation for the future of the EV industry.

In the 1990s, spurred on by growing concerns about climate change the idea of EVs began to build pace. The 1997 Kyoto Protocol helped solidify this as state parties committed to reduce greenhouse gas emissions.

Notably, GM released the EV1 its first EV, however the project faced significant technical and commercial challenges.

The 21st century brought the breakthrough that EVs needed, the development of lithium-ion batteries that suited their use case. With significantly higher energy density, longer lifespans, and faster charging capabilities, these batteries transformed the practicality and appeal of EVs. It was during this period that Tesla emerged as a major player.

Following the global financial crash of 2008 some countries began to view the industry as a strategic way to revitalise their economies while addressing environmental and energy security concerns.

This “green recovery” saw EVs emerge as a symbol of innovation, sustainability, and economic resilience, with countries adopting tailored strategies to support their transition. China led the way, investing heavily in EV subsidies, charging infrastructure, and battery R&D. It aimed to address poor air quality in its cities and grow its economy.

In the US, the American Recovery and Reinvestment Act of 2009 allocated billions to clean energy, EV subsidies, and infrastructure, helping companies such as Tesla and General Motors revitalise the American auto industry.

The EU used aggressive emissions targets as its foundation to fund EV research and support automakers in transitioning to EV production, particularly in Germany and France.

Meanwhile, Japan and South Korea focused on heavily on battery innovation, leading to Panasonic and LG Chem emerging as leaders in the global battery supply chain.

In the 2010’s many governments put subsidies in place to incentive consumers to switch to EVs, thus beginning the decarbonisation of their transport sectors.

What does the current EV & battery market look like?

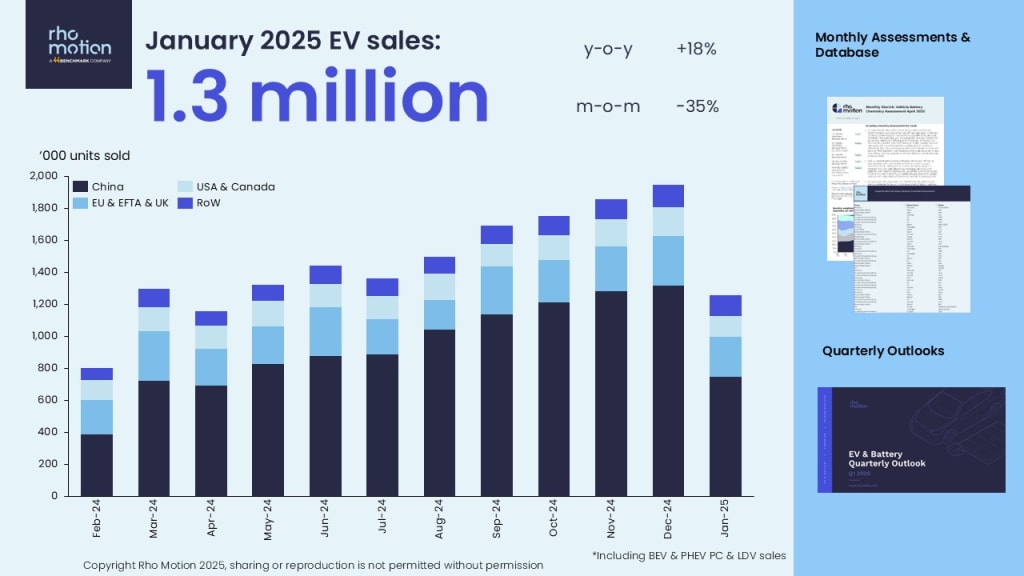

The EV market has evolved rapidly in recent years with annual EV sales reaching into the tens of millions. It is spread across three key regions, China, Europe and North America.

China dominates the market accounting for well over half of total global EV sales, Europe has the next largest demand for EVs follow by North America. Other markets are emerging in the rest of the world such as countries in Southeast Asia, Asia minor and South America however these only make up a smaller proportion of total demand but none the less have shown strong growth during the 2020s.

Considering the batteries that go into EV, the top ten lithium-ion battery producers’ control over 90% of the total market with CATL, BYD, and LG Energy Solution being the largest. All of the top ten players hail from either China, South Korea or Japan subsequently each of these respective countries have notable manufacturing capabilities, especially China. However as the industry has grown most companies have, and are establishing production facilities abroad, all over the world, either independently or with local partners such as automotive companies.

Notably geopolitical tensions are playing out in the EV and battery industries as these sectors grow. Various governments have put tariffs on Chinese imported EVs, while others are fearful of becoming too reliant on Chinese technology. Likewise, China is also wary about sharing some of its technologies with other countries.

EV demand has shown the strongest growth in China in recent years, driven predominantly by EV sales, and to a lesser extent BESS deployments. North America and Europe, both growing markets, however at more of subdued rate.

What is driving the EV & battery markets?

Subsidies have been key at driving EV adoption, helping to reduce the overall cost of buying an EV. However, many countries have now phased out subsides. Notably China phased out its subsidy in 2022, while in Europe only a handful of counties have direct subsidies for buying an EV, but many still offer incentives through tax pauses.

The US has an EV subsidy in the form of a tax credit reaching up to USD7,500 made possible through the IRA, however the future of this has come into question under President Trump.

With or without incentives and subsidies, price remains the biggest factor for driving EV sales. In China, most EVs have now reached price parity with ICE alternatives, and some EVs are cheaper than ICE alternatives this has been key at growing demand for EVs there.

In comparison to Europe, an EV costs on average approximately twice as much as an ICE alternative, while in the US this is approximately 1.5 times as much compared to an ICE alternative.

With price being a key driving factor, there are many reasons why China has reached cost parity, and the US and Europe have not. Largely it comes down to the battery, which makes up around 50% of the total cost of the EV.

EVs made in China tend to have cheaper batteries, firstly due to chemistry. The dominance of LFP in China means that battery prices are lower as the materials to make the battery are cheaper in comparison to NCM batteries. Secondly, Chinese vehicles tend to have smaller pack sizes compared to US and European vehicles, meaning the batteries are not as big and therefore not as expensive. This links with China’s extensive charging sector allowing consumers easier use of EVs. Lastly, in China production costs are far lower to what they are in Europe or the US meaning again the vehicles and batteries can be made more cheaply bringing down overall costs.

Price is a key driver for consumers, but legislation also has a factor to play. Within the EU, strict vehicle emission legislation mandate how much CO2 a vehicle can release, eventually trending towards 100% zero emission vehicles by 2035. These legislations drive vehicles sales across the bloc. Similarly, the UK has strict legislation tending towards the phase out of ICE vehicle sales by 2035.

While the US lacks any nationwide ban on ICE vehicles, various states have legislated their own targets towards the phase out of ICE vehicle sales including California that from 2035 will ban sales of non-ZEVs.

Lastly vehicle usage price must also be considered, this includes the price of charging an EV. For many, an EV presents the opportunity to reduce on going transport costs through the price of charging. While this remains true in many countries, some countries, especially in Europe have seen spikes in electricity prices which has eroded the benefit of lower on going costs to some extent. As well as this, charge point availability can also affect consumers attitude towards EVs inducing range anxiety, the fear that the vehicle battery will run out before finding a suitable charge point. China has broad coverage of EV chargers, while other countries lag behind with less coverage.

Who are the key market players shaping the EV industry?

As the EV market has expanded, a diverse set of players have emerged to dominate the landscape. These include legacy OEMs with established histories in ICE vehicles and a newer cohort of entrants with little to no ties to traditional automotive production. Similarly, the battery industry has been shaped by dominant global players and emerging challengers.

Europe

In Europe, legacy automakers have been key in driving the EV market forward. Companies such as the Volkswagen Group, Stellantis, Renault, BMW, and Volvo (under Geely ownership) have used their manufacturing capabilities and brand recognition to begin the transition from ICE vehicles to a more electrified portfolio. These players offer a wide range of options, including HEVs, PHEVs, and BEVs. Additionally, many of these players have announced electrification targets aiming to sell a certain number of electrified vehicles by certain dates.

North America

In North America, the EV market narrative is dominated by new entrants, with Tesla leading the way. Telsa accounts for the majority of the EV sales in the region with its Model 3 and Model Y vehicles widely recognised. However, legacy automakers such as General Motors and Ford have ramped up their EV strategies beginning to offer more EV models to the growing market in the region.

Tesla’s success has also spurred the emergence of additional startups such as Rivian and Lucid Motors, which are targeting niche segments. These companies, though nascent, are proving notable players within the industry.

China

China, presents a different dynamic with a mixture of legacy players and new brands. While established automakers such as SAIC and Geely have contributed to the sector’s growth, the spotlight increasingly falls on rising domestic players. BYD, for example, has not only become a major EV manufacturer but also a leader in battery production. Other prominent names such as NIO, Xpeng Motors, and Li Auto have also rapidly gained market share, leveraging advanced technologies, state-backed subsidies, and an understanding of domestic consumer preferences.

Who are the key players in the battery industry?

The battery industry is dominated by a handful of global giants. Companies such as Samsung SDI LG Energy Solution, Panasonic, CATL or BYD have established themselves as the leaders in battery cell production. These firms provide batteries not only to their domestic markets but also to global OEMs, forming a key part of the EV supply chain. All of these players have supply agreements with multiple OEMs across multiple regions.

Notably BYD follows a vertically integrated model, producing batteries not only for its own vehicles but also other players allowing to have a wide control of the market.

What are the main challenges to the EV and battery industry?

As the EV and battery industries continue to grow, these industries also face challenges. From geopolitical tensions affecting supply chains to scepticism over the reliability of new technologies, these hurdles have the potential to shape the industry’s trajectory.

How do geopolitics and supply chain vulnerabilities affect the industry?

The global EV and battery industries are deeply entwined with geopolitics, particularly because of their reliance on raw materials, critical components and new technologies.

Lithium, cobalt, nickel, and rare earth elements, essential for battery production, are often sourced from politically sensitive or resource-constrained regions. Similarly, dominance over the processing and refining of critical minerals affects the wider battery and EV markets as countries look to domesticise these industries.

China dominates the processing and refining of many critical minerals, giving it substantial leverage over the global supply chain.

This reliance on specific regions creates vulnerabilities for manufacturers. Trade tensions between China, Europe, and the US have increased pressure on automakers and battery producers to secure their supply chains. For example, the US’s IRA includes incentives for sourcing battery materials domestically or from friendlier nations, encouraging manufacturers to diversify away from China. However, reshoring or near-shoring supply chains is both capital-intensive and time consuming, making it a significant hurdle for the industry.

Energy security and geopolitical shocks also play a role in shaping the EV market. For example, the war in Ukraine has disrupted energy markets globally, indirectly affecting EV production costs by increasing the price of electricity in certain regions. Meanwhile, rising geopolitical competition over EV-related technologies such as battery patents and manufacturing processes may further complicate international collaboration and investment.

Scepticism towards new technologies

Despite the growing adoption of EVs, scepticism surrounding their technology and long-term sustainability continues to act as a barrier to widespread acceptance. This scepticism stems from a range of concerns, including the environmental impact of battery production, vehicle range limitations, charging infrastructure, and questions around long-term reliability. However, as EVs usage becomes more widespread spread many of these scepticisms are being eroded.

What opportunities lie in new technolgies?

The battery and EV industries are constantly evolving offering new opportunities within markets. There are now a broad range of ways to incorporate batteries into EVs which aim to improve space utilisation and reduce overall costs. Many players now use cell-to-pack technology that eliminates the need for battery modules by integrating cells directly into the battery pack. Other players are starting to use cell-to-chassis technology which integrates battery cells directly into the vehicle’s chassis, removing the need for a separate battery pack.

Further developments are seen in the chemistry and types of batteries used in vehicles. Solid state batteries and semisolid state batteries which offer improved safety and higher energy densities are being researched for future EV models.

As well as this, new battery chemistries are being developed and used such as sodium-ion, lithium-sulphur, and lithium manganese iron phosphate (LMFP).

These new designs, formats, and chemistries present future opportunities in the EV and battery landscapes, directing investment and thoughts towards avenues for further potential growth.