The transformation of the US battery industry began in 2014 with Tesla’s announcement of its first gigafactory, developed in collaboration with Panasonic, in Reno, Nevada. This marked the start of a journey towards the electrification landscape we see today. As the global automotive sector increasingly embraces electrification, investment in the US battery industry has gradually picked up pace. However, substantial growth only materialised after the Inflation Reduction Act (IRA) was signed into law in August 2022.

With federal support through tax credits and grants, the US battery industry experienced rapid expansion in the number of announced investments. Here, we explore the evolution of the Battery Belt, its current composition, and the factors likely to shape its future.

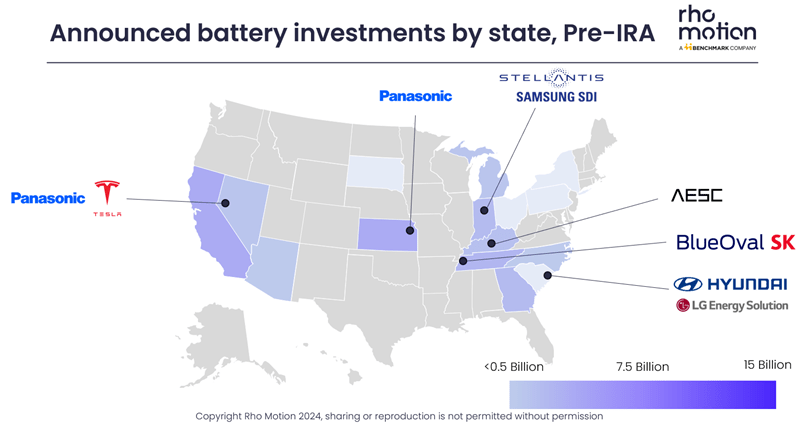

Laying the foundations of the Battery Belt

Before the IRA, battery investment was spread across the US, with early facilities established in California, Arizona, and Nevada. States like Kansas and others in the East, including Michigan, Illinois, Kentucky, Tennessee, North and South Carolina, and Georgia, also attracted significant projects. These initial investments formed the foundation of what is now referred to as the “Battery Belt.”

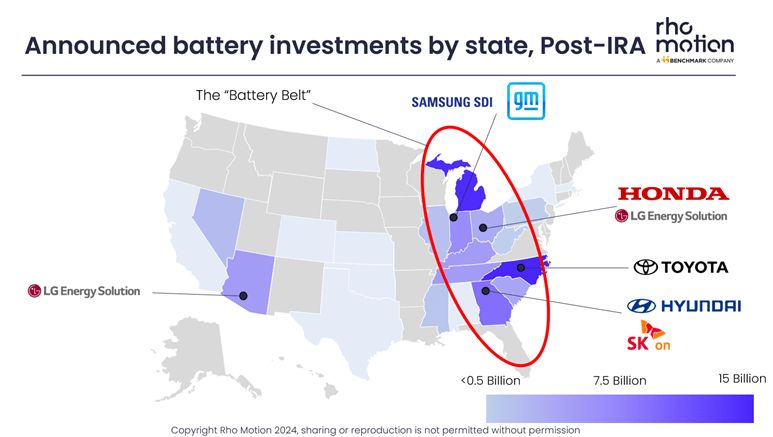

Cementing the Battery Belt’s location

The IRA’s enactment solidified the Battery Belt’s location in the Southeast and Midwest regions of the US. Federal financial incentives made these areas increasingly attractive to companies eager to capitalise on electrification. But why did these regions dominate? The answer lies in a blend of historical legacy and strategic advantages.

The Midwest, reviving an industrial heartland

Historically, the Midwest was the industrial hub of the US, home to key players like Ford, GM, and Chrysler in cities such as Detroit, Michigan. The region was a centre for the automotive and steel industries during the 20th century. However, deindustrialisation, global competition, and automation led to economic decline, with abandoned factories and high unemployment characterising the late 20th century.

Despite these challenges, automakers have maintained scaled-down operations in the Midwest. Electrification has offered an opportunity for reindustrialisation, prompting legacy companies such as GM, Ford, and Stellantis (owner of Chrysler) to base some of their electrification efforts in their historic home region.

Read: Europe’s EV subsidy landscape set for changes in 2025

The Southeast, a competitive challenger

While the Midwest leveraged its automotive heritage, Southern states such as North Carolina, South Carolina, Georgia, and Tennessee emerged as strong competitors. These states offered aggressive incentives, including tax credits, grants, and workforce training programmes, to attract EV and battery manufacturers. Georgia secured investments from Hyundai and Rivian with property tax abatements. North Carolina provided Toyota with USD271 million in incentives. South Carolina used job development credits, while Tennessee supported Ford’s BlueOval City with tailored aid and site preparation.

However, similarly the Midwest has offered similar incentives. Michigan granted USD600 million to Ultium Cells, Ohio supported LG Energy with workforce funding, and Illinois introduced the REV Act to encourage investments like Rivian’s factory expansion. However, the Southeast’s lower unionisation rates and reduced labour costs has given it an edge. According to the Bureau of Labour Statistics, on average 11.5% of workers in the Midwest belong to unions, compared to just 3.9% in the South. This difference impacts wage rates. The Bureau of Labour Statistics reports 39% higher average hourly wage for unionised blue-collar jobs, making labour in the Midwest significantly more expensive.

Strategic location and global supply chains

The Southeast’s proximity to major ports, including Charleston, Savannah, and Jacksonville, offers another advantage for the battery and EV industry, which relies on global supply chains for raw materials, components, and exports. In contrast, the Midwest’s nearest container ports, New York, Baltimore, and Virginia, are further away, adding to transport costs and times.

Proximity to EV manufacturing facilities is another key consideration. Ford, Stellantis, and GM operate the majority of their BEV and PHEV manufacturing facilities in the Midwest. These facilities are supported by nearby gigafactories such as Ultium, LG Energy Solution, and Samsung SDI, often established through joint ventures with automakers.

However, the Southeast has seen players including BMW, Volvo, Mercedes Benz, Nissan, VW, and Honda among others, choose the area to establish EV production facilities, targeting both the US market and the export market. Volvo and Mercedes Benz import a proportion of cells from CATL, while others rely on cells from players such as SK On, Samsung SDI and AESC. While some of these cells are acquired from gigafactories further north, the Southeast is poised to benefit from increasingly localised supplies as new facilities come online in the coming years.

Read: What the Trump Presidency means for the EV and battery industry

What’s next for the Battery Belt?

The future of the Battery Belt faces uncertainty as political winds shift. President-elect Donald Trump’s administration is likely to prioritise fossil fuels and ease environmental regulations, potentially impacting aspects of the IRA. Despite these higher-level aims, bringing manufacturing to the US and job generation will remain central to next administration. A full repeal of the IRA seems unlikely, however targeted changes such as revoking the 30D tax credit (worth up to USD7,500 for EV purchases) and rewriting EPA emissions rules could slow EV adoption. The recent Q4 release of the EV & Battery Quarterly Outlook saw US EV sales reductions of between 6 and 10% in the next six years. There is anticipation for further outlook reductions in the coming quarters dependent on decisions yet to be made.

Request: Rho Motion’s Q4 EV & Battery Quarterly Outlook Here

Since the IRA’s inception, over USD110 billion in EV and battery investments have flowed into the US, with 92% of these funds directed towards what are now Republican-led state s. Rolling back federal support could prove politically unpopular in these regions. Nevertheless, a slowdown in EV demand could delay or reduce investments in the Battery Belt.

Benchmark reports that 2024 has already seen record cancellations of gigafactory capacity globally, amounting to 312GWh. However, the US is expected to bring 160GWh of new manufacturing capacity online in 2025.

The US battery industry continues to evolve rapidly, with the Battery Belt firmly established as its hub. While political and market uncertainties may influence the pace of development, the momentum built since the IRA’s passage suggests the Battery Belt will remain a critical pillar of the EV and battery revolution.

More information

For more information about the battery landscape, see our research or get in touch.